The big news in the crowdfunding sector in March 2026 was the collapse of the UK-based craft beer company BrewDog. In a series of equity crowdfunding rounds spanning more than a decade, over 220,000 retail investors had put approximately £75 million into the business. They called themselves “Equity Punks.” They believed they were joining a revolution. When the end came, they were left with nothing.

The Rise of “Community Capitalism”

BrewDog’s “Equity for Punks” model was genuinely innovative when it launched in 2009. Online crowdfunding was very new, and it allowed ordinary consumers to invest directly in a fast-growing consumer brand. The pitch blended investment with belonging. Shareholders received perks such as discounts in BrewDog bars, invitations to shareholder events and exclusive beers brewed for investors. Some enthusiasts went further, getting BrewDog tattoos that entitled them to lifetime discounts. In effect, BrewDog blurred the line between a loyalty programme and an equity investment. Fans became shareholders, and shareholders became brand ambassadors.

The founders had vowed to never spend a penny on paid-for advertising. Though they happily hired and branded a helicopter to make a video of parachuting “fat cats” (stuffed toys, I hasten to add) into the City of London to generate news coverage of the fact that they were crowdfunding. This first round of BrewDog crowdfunding went on to raise their first £5m – without the services of any expensive “fat cat” investment advisers.

The fledgling brand set a fundraising example that inspired several other brewers to go down the crowdfunding route, and whether they brewed craft or traditional beer didn’t seem to matter.

BrewDog’s blurring of identity and investment was, with hindsight, one of the central dangers of the whole enterprise. Their fundraising and generally irreverent marketing blurred the line between investment and identity. Investors were not just buying shares — they were buying into a movement. One time, to publicise opening a bar in north London, they hired a tank to motor through the streets of Camden.

As Dr Hadar Gafni, a lecturer in entrepreneurial finance at King’s College London, has pointed out, that distinction between investment and identity matters enormously: when people invest in a story rather than a set of financial fundamentals, they tend to ask fewer difficult questions. Is the company profitable? What protections do shareholders have? What happens if things go wrong?

The Annual General Meeting, typically a key moment for accountability, took the form of a music festival atmosphere. Investors who loved the brand were less inclined to scrutinise the financial structure behind their investment, or to fully understand it. BrewDog’s highly dispersed base of small retail investors had little collective power to influence the company’s direction. They were, as Dr Gafni put it bluntly, passengers.

The Deal That Changed Everything

In 2017, the two co-founders struck a deal with TSG Consumer Partners, a US private equity firm. TSG invested £213 million in BrewDog for a roughly 22% stake. The deal made the founders multimillionaires overnight — both James Watt and Martin Dickie reportedly pocketed around £50 million each from the transaction.

But the terms of that deal contained a structural time bomb for everyone else. TSG’s shares carried a liquidation preference and an 18% annual compound return, ensuring the firm would be paid ahead of ordinary shareholders. While this kind of arrangement is common in private equity, the consequence for BrewDog’s retail investors was profound: the bar for them to see any meaningful return was set extraordinarily high from that moment on. The “Equity Punks” had, knowingly or not, accepted a position at the back of the queue.

The compounding arithmetic was merciless. By 2024, the private equity firm was reportedly owed more than £700 million under the terms of the deal, alongside significant additional loans. The business was already in chronic decline. The gap between what TSG was owed and what the business was actually worth had become unbridgeable.

Chasing the Unicorn

In the years following the TSG deal, BrewDog’s ambitions became increasingly global. The company opened flagship bars around the world, launched hotels, expanded into spirits and continued promoting headline-grabbing marketing campaigns. Watt framed the strategy bluntly: BrewDog would either become a global success or “crash and burn.” Revenues grew rapidly and valuations were at one point claimed to reach £1.8 billion. But expansion proved ruinously expensive, and profitability remained elusive.

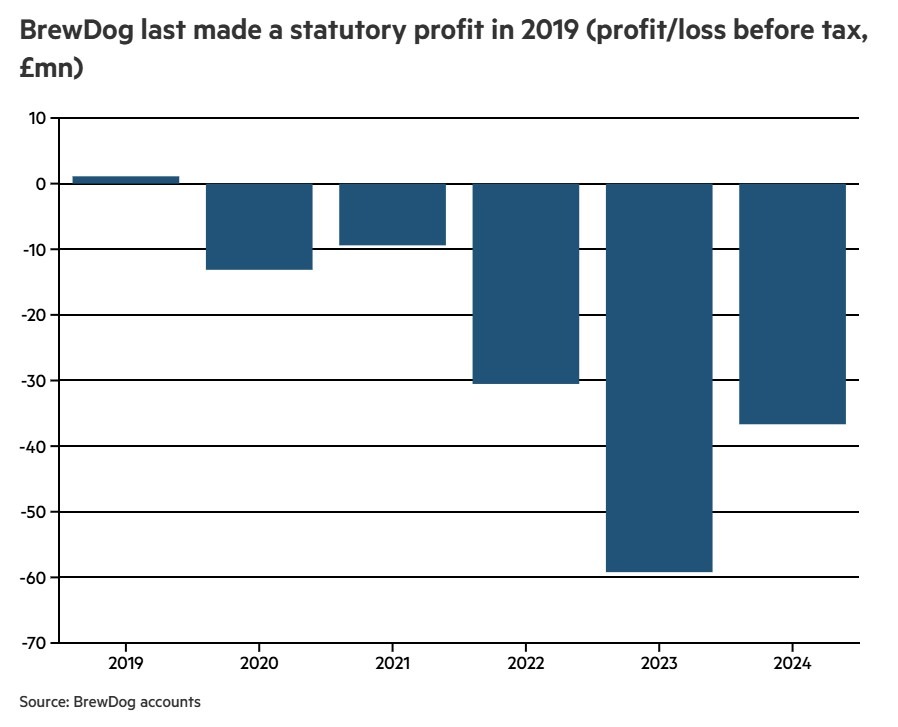

The company had last recorded a profit in 2019. BrewDog’s expansion-at-any-cost strategy, fuelled by significant amounts of debt, came home to roost quite spectacularly. Its share of UK beer sales never exceeded 5%. The question that goes largely unanswered is why a business with such a modest domestic market position felt justified in attempting to expand to as many as 100 venues globally. Ambitious debt-fuelled expansion plans, coupled with expensive flagship properties, proved unsustainable.

By late 2025, when both co-founders had departed the business within a year of each other — a development that left the writing clearly on the wall — the company was well on its way to recording a total loss approaching £500 million. When a company reaches that point, the fate of ordinary shareholders is essentially sealed.

The Collapse and Its Human Cost

The company was placed into administration and, having at one time been valued at over $1 billion, was acquired for just £33 million by US cannabis and wellness company Tilray Brands. The acquisition covered BrewDog’s global brand, intellectual property, UK brewing operations, and 11 top-performing venues, leaving behind the majority of the unprofitable bar estate and nearly 500 jobs. A total of 484 BrewDog employees were made redundant, breweries around the world were offloaded, and 38 bars were shut down.

Tilray CEO Irwin Simon has claimed the redundancies had “nothing to do with” them, and the company has suggested it is exploring franchising opportunities that could see some bars reopen under new operators. Whether that materialises remains to be seen. The immediate reality for nearly 500 workers — and for the communities that had invested in both the brand and the business — was stark.

For BrewDog’s retail investors, the outcome was complete. More than 200,000 retail investors, BrewDog’s self-styled “equity punks”, had collectively invested around £75 million into the company. They received perks, discounts and a sense of belonging. What they did not receive was any return when the company was sold. A few years of discounted products were the only tangible financial benefit most of them ever enjoyed.

What the Research Tells Us

The BrewDog story is not unique in the crowdfunding world, but it is unusually vivid. Entrepreneurial finance lecturer Dr Gafni, who has been researching crowd-based investment alongside colleagues at Copenhagen Business School, offers a measured but important observation. The finding is not that crowds are irrational. In fact, they can be remarkably good at separating promising investments from poor ones — but only under the right conditions. Investors need access to clear financial information and a diversity of perspectives.

When a pitch leans heavily on community, identity or shared values, investors tend to make more aligned rather than diverse assessments. Enthusiasm becomes contagious. Critical judgement is crowded out.BrewDog was a textbook case. The very things that made it such a compelling fundraising vehicle — the culture, the community, the anti-establishment energy — were the things that made its investors least likely to ask the hard questions that might have protected them.

What Needs to Change

The collapse has renewed calls for tighter regulation of equity crowdfunding, and the debate is a live one. Critics have long pointed to the sector’s structural weaknesses: investments in businesses with inflated valuations; shares that are highly illiquid and extremely difficult to trade; the vulnerability of retail investors to terms struck with later institutional investors who move to the front of the repayment queue; and the limited accountability structures of privately owned companies with dispersed ownership bases.

The more important issue, however, may be one of design rather than simply regulation. If companies want to raise money from retail investors, the risks need to be impossible to miss, not buried in small print. Financial information should be standardised, prominent and clearly separated from marketing. At present, there is often no effective barrier between the two.

Retail investors should also recognise that share ownership carries governance implications: when a company’s ownership is fragmented among thousands of small shareholders, meaningful oversight of management can be weak or effectively absent. Liquidity is another factor that deserves far more prominence in how crowdfunded investments are presented. Shares in crowdfunded companies are typically difficult to sell, meaning investors may have to hold them for years with little ability to exit. In BrewDog’s case, shareholders could trade their shares only occasionally through a specialised platform, and even then there was no guarantee of finding a buyer.

The Lessons for Investors

Some say equity crowdfunding has always carried these risks: illiquid positions; inflated valuations; susceptibility to institutional deals that demote retail investors; and limited recourse against unregulated private company founders. Some want it more tightly regulated. Both positions have merit.

But for investors who had been sitting on a valuable paper profit, the most personal and actionable lessons are different. Never take a paper valuation for granted, and never treat a crowdfunded investment as something you can simply file away and forget. BrewDog’s annual reports showed clearly that the company had not made a profit since 2019. That information was available to anyone paying attention.

The final chance to take advantage of a share buy-back scheme had been in 2022. That provided a window of at least three years in which a paying-attention investor could have made a decision to realise at least some level of return before the end came. The question worth asking — uncomfortably — is how many Equity Punks were actually watching.

Crowdfunding can work. It has genuinely helped hundreds of businesses reach early-stage capital they could not have accessed through conventional routes. But it requires investors who approach it with the same discipline they would bring to any other financial decision: read the accounts, understand the capital structure, know who gets paid first if things go wrong, and recognise that loyalty to a brand and sound investment practice are two very different things.