We’ve all seen the clickbait media headlines about AI’s impact on recruitment policies. Growing levels of graduates cannot find what they consider to be appropriate employment, at the same time as many companies are scaling down the places available on their graduate training schemes. How about the people already in what appears to be a successful career? In how many instances will AI force career changes.

Many parents may see their grown-up kids facing this situation after leaving uni, and saddled with debt. But before long, it could be impacting them directly as well.

A growing body of research suggests that AI isn’t simply automating the bottom of the labour pyramid. It’s climbing fast, and some of its steepest gains are happening precisely in the cognitive, analytical, and communicative tasks that define senior business roles. Younger workers are adapting. Retirees are out of the equation. In between, executives and managers aged 40 and over, who have built careers on expertise, judgement, and institutional knowledge, may be facing the most disorienting disruption of all.

You’re 47, 52, or 57 years old. You’ve spent two decades or more earning seniority the hard way: reading markets, managing teams, navigating boardrooms, and developing the kind of judgment that can’t be learned from a course.

You’re not naive about AI. You’ve read the headlines, sat through the strategy decks, maybe even signed off on a few AI pilots in your department. You assumed the disruption would happen below you, to people with the more routine roles involving repetitive work.

You thought you were safe from AI because you have built a value proposition based on three pillars:

depth of domain expertise,

a network of professional relationships,

judgment that comes from years of pattern recognition.

All three are real and hard-won. All three are also, to varying degrees, being replicated or replaced by AI tools available to anyone with an internet connection. This means many things are going to change, and many people will face the demands and turmoil of a drastic career change.

It seems an appropriate time for me to blow the dust off a set of 10 recommendations on how to manage a career change. I wrote and published this list over 10 years ago after attending an event covering the challenges facing former company directors who were changing career – not necessarily of their own choice – to ‘go it alone’. This could mean starting a new business, investing in other people’s new businesses, or taking interim roles to guide companies unable to afford their experience and knowledge on a full-time basis.

It’s scary to be in a new place. Doing new things, outside of a comfort zone that may have previously been full of support, is very tough.

Many of your previous contacts become useless after a career change because they were part of that former comfort zone, that former life.

It’s difficult to achieve a target daily pay rate, so do what comes up that looks like it would be good to be involved with.

Don’t forget that time is your most precious asset, particularly if you are starting a new enterprise later in life.

Reconsider the people who you know. Build connections among a new group of people who are going to be able to help the new you.

Think also about how to help them, not only how they could help you. Support is a two-way street.

Remain curious and love learning, which is now easier than it ever was.

Add practice to your knowledge, by simply getting out there to start providing others with the benefits of your knowledge and skills. Even do it free for a local charity or good cause rather than keep them to yourself. This will help teach you how to best present that knowledge in a way that builds confidence.

Confidence is what your new customers or investors will recognise and buy in to.

Work with people you like, who respect you and pay you on time. Life’s too short to do otherwise.

I would now add to this list, learn to use AI tools that will maximise your efficiency and multiply your effectiveness to prospective clients. AI by itself doesn’t take jobs away. People who use AI will replace people who don’t.

For some people it can represent liberation, freedom to pursue personal ambitions rather than play it safe. It worked that way for Nik Storonsky, the co-founder of Revolut. He was one of the former workers at Lehmann Brothers in Canary Wharf. One of the people carrying their personal items in a cardboard box as they left the building for the last time after it collapsed in the global financial crash in 2008.

He had experienced the delays and excessive fees for changing currency for his numerous business trips, and his family visits back to Moscow. He came up with Revolut, and ran some early stage crowdfudning to get the ball rolling. Today, Revolut has over 70 million customers, supports money transfers across more than 160 countries and regions, and it was valued at $75 billion in November 2025.

If you have ideas of what you want to do and achieve, and crowdfunding could be a source of finance for your startup, please drop me a line or give me a call. Let’s see how much I can help and support you. I am an independent crowdfunding advisor, without the restriction of ties to any specific crowdfunding platform.

The big news in the crowdfunding sector in March 2026 was the collapse of the UK-based craft beer company BrewDog. In a series of equity crowdfunding rounds spanning more than a decade, over 220,000 retail investors had put approximately £75 million into the business. They called themselves “Equity Punks.” They believed they were joining a revolution. When the end came, they were left with nothing.

The Rise of “Community Capitalism”

BrewDog’s “Equity for Punks” model was genuinely innovative when it launched in 2009. Online crowdfunding was very new, and it allowed ordinary consumers to invest directly in a fast-growing consumer brand. The pitch blended investment with belonging. Shareholders received perks such as discounts in BrewDog bars, invitations to shareholder events and exclusive beers brewed for investors. Some enthusiasts went further, getting BrewDog tattoos that entitled them to lifetime discounts. In effect, BrewDog blurred the line between a loyalty programme and an equity investment. Fans became shareholders, and shareholders became brand ambassadors.

The founders had vowed to never spend a penny on paid-for advertising. Though they happily hired and branded a helicopter to make a video of parachuting “fat cats” (stuffed toys, I hasten to add) into the City of London to generate news coverage of the fact that they were crowdfunding. This first round of BrewDog crowdfunding went on to raise their first £5m – without the services of any expensive “fat cat” investment advisers.

The fledgling brand set a fundraising example that inspired several other brewers to go down the crowdfunding route, and whether they brewed craft or traditional beer didn’t seem to matter.

BrewDog’s blurring of identity and investment was, with hindsight, one of the central dangers of the whole enterprise. Their fundraising and generally irreverent marketing blurred the line between investment and identity. Investors were not just buying shares — they were buying into a movement. One time, to publicise opening a bar in north London, they hired a tank to motor through the streets of Camden.

As Dr Hadar Gafni, a lecturer in entrepreneurial finance at King’s College London, has pointed out, that distinction between investment and identity matters enormously: when people invest in a story rather than a set of financial fundamentals, they tend to ask fewer difficult questions. Is the company profitable? What protections do shareholders have? What happens if things go wrong?

The Annual General Meeting, typically a key moment for accountability, took the form of a music festival atmosphere. Investors who loved the brand were less inclined to scrutinise the financial structure behind their investment, or to fully understand it. BrewDog’s highly dispersed base of small retail investors had little collective power to influence the company’s direction. They were, as Dr Gafni put it bluntly, passengers.

The Deal That Changed Everything

In 2017, the two co-founders struck a deal with TSG Consumer Partners, a US private equity firm. TSG invested £213 million in BrewDog for a roughly 22% stake. The deal made the founders multimillionaires overnight — both James Watt and Martin Dickie reportedly pocketed around £50 million each from the transaction.

But the terms of that deal contained a structural time bomb for everyone else. TSG’s shares carried a liquidation preference and an 18% annual compound return, ensuring the firm would be paid ahead of ordinary shareholders. While this kind of arrangement is common in private equity, the consequence for BrewDog’s retail investors was profound: the bar for them to see any meaningful return was set extraordinarily high from that moment on. The “Equity Punks” had, knowingly or not, accepted a position at the back of the queue.

The compounding arithmetic was merciless. By 2024, the private equity firm was reportedly owed more than £700 million under the terms of the deal, alongside significant additional loans. The business was already in chronic decline. The gap between what TSG was owed and what the business was actually worth had become unbridgeable.

Chasing the Unicorn

In the years following the TSG deal, BrewDog’s ambitions became increasingly global. The company opened flagship bars around the world, launched hotels, expanded into spirits and continued promoting headline-grabbing marketing campaigns. Watt framed the strategy bluntly: BrewDog would either become a global success or “crash and burn.” Revenues grew rapidly and valuations were at one point claimed to reach £1.8 billion. But expansion proved ruinously expensive, and profitability remained elusive.

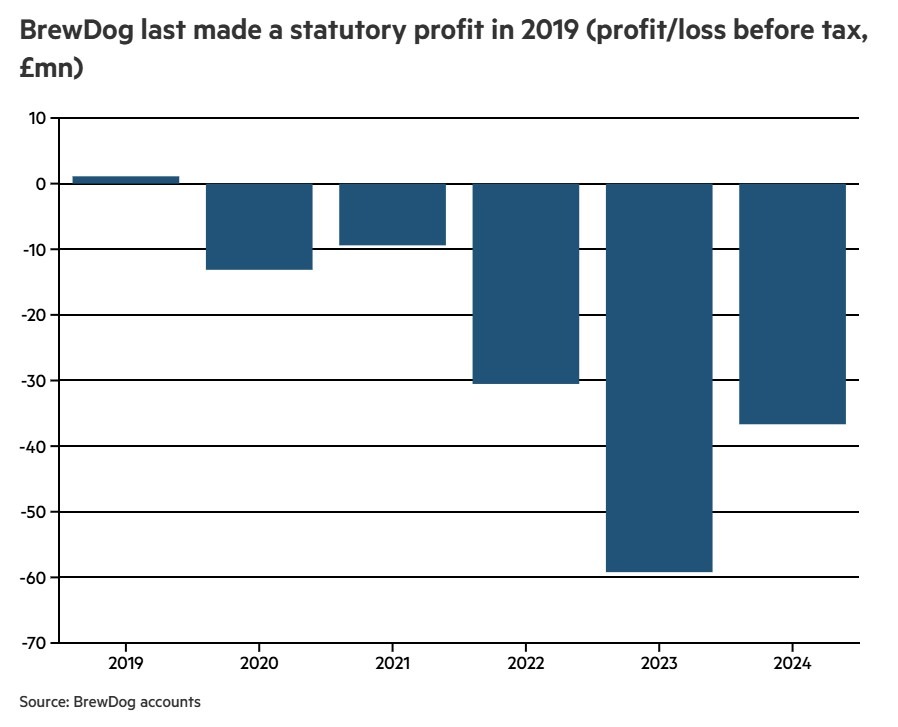

The company had last recorded a profit in 2019. BrewDog’s expansion-at-any-cost strategy, fuelled by significant amounts of debt, came home to roost quite spectacularly. Its share of UK beer sales never exceeded 5%. The question that goes largely unanswered is why a business with such a modest domestic market position felt justified in attempting to expand to as many as 100 venues globally. Ambitious debt-fuelled expansion plans, coupled with expensive flagship properties, proved unsustainable.

By late 2025, when both co-founders had departed the business within a year of each other — a development that left the writing clearly on the wall — the company was well on its way to recording a total loss approaching £500 million. When a company reaches that point, the fate of ordinary shareholders is essentially sealed.

The Collapse and Its Human Cost

The company was placed into administration and, having at one time been valued at over $1 billion, was acquired for just £33 million by US cannabis and wellness company Tilray Brands. The acquisition covered BrewDog’s global brand, intellectual property, UK brewing operations, and 11 top-performing venues, leaving behind the majority of the unprofitable bar estate and nearly 500 jobs. A total of 484 BrewDog employees were made redundant, breweries around the world were offloaded, and 38 bars were shut down.

Tilray CEO Irwin Simon has claimed the redundancies had “nothing to do with” them, and the company has suggested it is exploring franchising opportunities that could see some bars reopen under new operators. Whether that materialises remains to be seen. The immediate reality for nearly 500 workers — and for the communities that had invested in both the brand and the business — was stark.

For BrewDog’s retail investors, the outcome was complete. More than 200,000 retail investors, BrewDog’s self-styled “equity punks”, had collectively invested around £75 million into the company. They received perks, discounts and a sense of belonging. What they did not receive was any return when the company was sold. A few years of discounted products were the only tangible financial benefit most of them ever enjoyed.

What the Research Tells Us

The BrewDog story is not unique in the crowdfunding world, but it is unusually vivid. Entrepreneurial finance lecturer Dr Gafni, who has been researching crowd-based investment alongside colleagues at Copenhagen Business School, offers a measured but important observation. The finding is not that crowds are irrational. In fact, they can be remarkably good at separating promising investments from poor ones — but only under the right conditions. Investors need access to clear financial information and a diversity of perspectives.

When a pitch leans heavily on community, identity or shared values, investors tend to make more aligned rather than diverse assessments. Enthusiasm becomes contagious. Critical judgement is crowded out.BrewDog was a textbook case. The very things that made it such a compelling fundraising vehicle — the culture, the community, the anti-establishment energy — were the things that made its investors least likely to ask the hard questions that might have protected them.

What Needs to Change

The collapse has renewed calls for tighter regulation of equity crowdfunding, and the debate is a live one. Critics have long pointed to the sector’s structural weaknesses: investments in businesses with inflated valuations; shares that are highly illiquid and extremely difficult to trade; the vulnerability of retail investors to terms struck with later institutional investors who move to the front of the repayment queue; and the limited accountability structures of privately owned companies with dispersed ownership bases.

The more important issue, however, may be one of design rather than simply regulation. If companies want to raise money from retail investors, the risks need to be impossible to miss, not buried in small print. Financial information should be standardised, prominent and clearly separated from marketing. At present, there is often no effective barrier between the two.

Retail investors should also recognise that share ownership carries governance implications: when a company’s ownership is fragmented among thousands of small shareholders, meaningful oversight of management can be weak or effectively absent. Liquidity is another factor that deserves far more prominence in how crowdfunded investments are presented. Shares in crowdfunded companies are typically difficult to sell, meaning investors may have to hold them for years with little ability to exit. In BrewDog’s case, shareholders could trade their shares only occasionally through a specialised platform, and even then there was no guarantee of finding a buyer.

The Lessons for Investors

Some say equity crowdfunding has always carried these risks: illiquid positions; inflated valuations; susceptibility to institutional deals that demote retail investors; and limited recourse against unregulated private company founders. Some want it more tightly regulated. Both positions have merit.

But for investors who had been sitting on a valuable paper profit, the most personal and actionable lessons are different. Never take a paper valuation for granted, and never treat a crowdfunded investment as something you can simply file away and forget. BrewDog’s annual reports showed clearly that the company had not made a profit since 2019. That information was available to anyone paying attention.

The final chance to take advantage of a share buy-back scheme had been in 2022. That provided a window of at least three years in which a paying-attention investor could have made a decision to realise at least some level of return before the end came. The question worth asking — uncomfortably — is how many Equity Punks were actually watching.

Crowdfunding can work. It has genuinely helped hundreds of businesses reach early-stage capital they could not have accessed through conventional routes. But it requires investors who approach it with the same discipline they would bring to any other financial decision: read the accounts, understand the capital structure, know who gets paid first if things go wrong, and recognise that loyalty to a brand and sound investment practice are two very different things.

It was a great pleasure to spend time last week at the EU Startups Summit in Malta. One particularly worthwhile session was a panel discussion on Equity Crowdfunding Dos and Don’ts. A panel of international experts began with a runthrough of the added benefits equity crowdfunding delivers beyond raising funds for early stage businesses to accelerate their growth. Their positivity clashed with a report on the current equity crowdfunding slump I came across on my return home.

Panellists, left to right: Mindaugas Valiulis – Policy Officer, European Commission; Grégoire Touazi – Legal Counsel, Crowdcube Europe; Nora Szeles – CEO, Tőkeportál; Christopher Burge – Co-Founder & CEO, Spark Crowdfunding; Oliver Gajda – Executive Director, Eurocrowd.

Their combined summery of added benefits included:

Successful crowdfunding shows that a business (not necessarily only startups) has the support of a crowd of believers.

A successful round provides social proof of a business worth backing

A crowdfunding investment round can act as a catalyst to unite a community behind a business opportunity, and give them a sense of identity and stronger belief.

Successful crowdfunding is good marketing – it gets a business noticed and talked about.

The best retail investors will support their investments with positive word-of-mouth as they progress up the brand loyalty ladder, becoming advocates and brand ambassadors, and may also become important customers as well.

Crowdfunding enables backers to meet business founders, which can lead to an exchange of introductions, and offers of insight, expertise and assistance.

Each subsequent round can build on the previous one(s), as investors scale up their investments over time.

Future raises have potential as private rounds, carried out exclusively among existing shareholders.

However, my return to the UK coincided with Bloomberg UK publishing an article on the current downturn in equity crowdfunding. The author wrote: “Weaker investor appetite, tough economic headwinds and a patchy success rate are making the [equity crowdfunding] model a tougher sell for both businesses and buyers.”

Data compiled by Beauhurst shows the degree of the downturn.

It got me thinking that when equity began in the UK in around 2012, there was a very low interest rate and there was very low inflation. Net Present Value calculations were hardly required when considering potential returns on investments.

Then in swift succession there was Brexit, Covid (with ‘quantitative easing’ = printing money), the follow-on global reassessment of startup values, a return of inflation, and now Trump’s deliberate destabilisation of global trading.

Aside from these global macro factors, there has been unsettling news within equity crowdfunding itself. This includes cases of businesses that had been funded through crowdfunding going in to administration, and then being bought back by the original founder who was then debt-free. Though the investments of the crowdfunding backers were wiped out and worthless. It’s difficult for investors and interested onlookers to see how this is fair. Thank you East London Liquor Company, among others. Or as they explain it, the blame should fall on HMRC for forcing the business into administration.

The UK Crowdfunding Association – formed to advance the crowdfunding and alternative finance industry – has been publicly silent, while some newspaper reader comments I came across showed the mood of disgruntled investors who responded to such reports with negativity and accusations of behaviour bordering criminality.

While platforms continue to consolidate, Eurocrowd recently commented that the ECSP Regulations intended to harmonise equity crowdfunding across the EU have failed to bring about an anticipated increase in the popularity and use made of equity crowdfunding.

Update

After originally publishing this article in April 2025, I later raised the matter on X/Twitter. My comment was picked up by Crowdfund Insider, who then published their own article on the topic in November 2025. Their answer, in summary, was: “It is a combination of factors, including questions about deal quality, risk aversion, and economic hurdles for smaller investors—such as rising taxes.”

There is also the growing level of rival opportunities for retail investors. The value of gold has risen by over 50% in the 12 months to 4 December 2025, and Bitcoin has provided investors with its usual rollercoaster of ups and downs. Casks of aged whisky and investments in works of art by up-and-coming artists are among the alternative options increasingly available today.

Is it any wonder there’s been a downturn and an equity crowdfunding slump? And where is there a voice that is championing crowdfunding as an effective means of delivering numerous other benefits on top of raising investment funds for privately-owned businesses?

This round-up shows the flexibility of crowdfunding for a wide range of users. They include organisations that were asking for donations, selling equity, and encouraging people to invest in community shares.

First, did you know women-led crowdfunding projects outperform men’s by success rate in achieving funding, with 20% shorter campaign completion times.

Equity Crowdfunding

Established in 2009, the made-to-order and sustainable fashion brand Wolf in Sheep’s Clothing (WISC) closed its equity crowdfunding campaign after beating its £150,000 target by 7%. The money will be used for marketing costs and new machinery.

The Smart Container Company is offering equity through crowdfunding to raise funds and accelerate the development of its smart beer kegs. IoT blockchain technology enables tracking their location and checking the temperature the contents is stored at. By February 28 the company had raised 112% of its £150,000 target with 22 days left to tun. EIS benefits (Enterprise Investment Scheme) are available for investors who are UK taxpayers.

JNCK Bakery offers low-sugar, nutritionally enhanced cookies, and recently launched in 550-plus stores across the UK. In February the fmcg startup closed an equity crowdfunding round after raising more than £260,000 to further accelerate growth.

Equity crowdfunding by Reality Games raised £1.56m to further develop an immersive geolocation and augmented reality version of the classic Monopoly board game. Players can explore their own city, trade virtual properties, and compete in global challenges.

UK healthtech startup MultiplAI Health is developing an AI and RNA-based screening test to detect earliest stage cardiovascular and complex diseases. By February 28, with 8 days left to run, MultiplAI Health had reached 71% of its £300,000 target to accelerate commercialising as a lab-developed test in the U.S. market.

Vegan fashion startup Immaculate Vegan, founded in 2019, raised £183,375 through equity crowdfunding from 114 investors. Its target was £150,000 to expand its women’s offering, build newer men’s, home, kids, beauty and pets categories, plus accelerate US customer growth.

A new night train service called “European Sleeper” has crowdfunded for a number of years and in total has raised over €5.5m from over 4,000 backers. The Sunday Times reported on one of its pilot journeys from Brussels to Venice, complete with passengers sleeping in refurbished carriages that are 50 or more year old.

Not at all such good news for investors in Gunna Drinks. The Grocer reported that the collapse of the premium soft drinks brand had left crowdfunding investors particularly angry. They hadn’t even been told the founder and CEO had stepped down last November. “Why are we always the last to know?” complained one exasperated backer.

On a happier note, two guys in Salford who have been friends since school launched The Salford Rum Company in 2018 with £5,000 of savings. Their premium rum rivals luxury gins, and they quickly raised over £314,000 from a round of equity crowdfunding. This has already beaten their £250,000 target and as from February 28 there’s still 26 days left to invest.

P2P Lending Through Bonds

British luxury home decor, wallpaper and lifestyle company, the B-Corp House of Hackney, is crowdfunding to raise £2 million by issuing fixed-interest bonds through Triodos Bank UK. It wants to buy out existing private equity shareholders and pursue its ESG commitments with more vigour. By February 28 it had raised just over £308,000 with 28 days left to run. Looks like it’s going to be a tough call.

Donations and Rewards Crowdfunding

Bramley Baths is an Edwardian heritage treasure in Leeds, and its fundraisers gave themselves until the end of February to raise the final balance of its community shares crowdfunding target of £350,000 to repair and restore the roof, while also installing new energy-saving features. By the time the crowdfunding project closed at 5pm on February 28 it had raised £374,360 from 531 investors in 140 days.

Community shares are an opportunity for people to champion a local organisation or community asset through financial investment. Community shares are unique to co-operatives and community benefit societies, and they can’t be sold to anyone else. Also, no matter how many shares anyone buys, each shareholder gets just one vote when it comes to making decisions.

A group of anaesthetists (doctors trained in anaesthesia) claim the General Medical Council has blurred the distinction between Doctors and Associates. They are crowdfunding to afford legal action against the GMC. It had raised £176,927 by February 28, and was scheduled to run for a further 30 days.

Aptitude Health & Fitness, a gym in Cheshire that launched during Covid, has gained permission to triple its size in new premises. In February the founder launched a crowdfunding campaign to raise £30,000 to meet some of the costs and also strengthen user loyalty. By February 28 he had raised over £17,600 with 16 days remaining.

The owners of Devon-based Sharpham Cheese, Greg and Nicky Parsons, hope their round of reward-based crowdfunding will raise £65,000 to enable them to invest in renewable energy, water recycling and new cheese making equipment.

Coming soon

In April I’ll be covering the EU-Startups Summit in Malta for Crowdsourcing Week and BOLD Awards. Two days of networking, inspiration, and learning includes 15 selected startups pitching to a panel of VCs and angel investors for funding. Find out more at https://eu-startups.com/summit/

In the meantime, if you have ideas and plans for using crowdfunding that you’d like to discuss with an impartial and independent crowdfunding adviser, please get in touch by email to [email protected].

The public round of voting in the global BOLD Awards for digital industries has closed. The next stage was an assessment by a judge from an international panel, and there are six finalists in the 2025 Boldest Crowdfunding Project category. They will all be invited to attend the gala dinner award ceremony in Lisbon on Friday March 28th, 2025. Crowdfunding is one of 33 categories of digital industries and the tech that powers them, and all category winners will be announced at the event.

Beyond successfully hitting their monetary target, BOLD Awards judges were looking for projects that were particularly effective in promoting their round of crowdfunding, and projects that derived other important benefits beyond raising funds.

Here is a rundown on the six finalists, and you can use the links to check out their BOLD Awards’ entry in full.

Body Rocket

Body Rocket provides bicycle add-ons for serious performance cyclists, including triathletes, to improve the aerodynamics of not only their bike set-up but also their body position. Pre-order sales on Kickstarter provided public validation of their products, and a round of equity crowdfunding enabled customers and other retail investors to be part of the business and enjoy the ride!

This Midlands-based bike maker is almost 100 years old, confirming that equity crowdfunding is not just for startups. Their crowdfunding project in 2023 accelerated development of a range of e-cargo bikes for last-mile delivery purposes, and e-bikes appropriate for public hire schemes. Their agreements with regional transport authorities, and an innovative tie-in with a large-scale residential property developer, ensured a ready market for their products. Their growing D2C sales cleverly involved introducing new owners to their dealers around the country for servicing and accessories.

Neurita is a range of fruit flavoured tequilas, at 35% ABV, designed to appeal more to female drinkers. A concerted effort by the startup founder enabled the brand to quickly win numerous plaudits and medals at international drinks trade shows. This product validation helped encourage investors to back her round of equity crowdfunding. Equally, the crowdfunding success will act as a marketing springboard to open the door to new distribution deals. Good crowdfunding is good marketing!

This chain of sustainable coffee shops based in Belgium began trading just four years ago from a single vintage truck. It now has 22 ‘bricks and mortar’ outlets, and the funds generated by a round of equity crowdfunding in 2024 will accelerate opening outlets in major cities throughout the EU. Any customer had an opportunity to become a shareholder.

The crowdfunding also recruited a cohort of highly brand loyal supporters. Backers who invested higher amounts were able to become accredited Brand Ambassadors. They will provide valuable word-of-mouth support about IzyCoffee’s sustainability priorities and behaviours in the locations of both the existing stores and where a new store will open in the next couple of years.

Prime Time brews award-winning, low-calorie beer in the UK. The two founders shared a passion for great tasting beer and good times. Their commitment to staying fit and leading a balanced lifestyle also led them to brewing beers that have 30% fewer calories, 63% fewer carbs, are gluten free and suitable for vegans.

Publicising their crowdfunding in 2024 was helped by having gained over 10,000 Instagram followers. A presence at festivals and other events also built brand exposure among sociable early adopters and provided opportunities to sign up new followers.

Added incentives to invest included a 20% discount off their website prices for every investor backing them to the tune of £100 or more, rising to 40% for £5,000 or more.

This Canadian entry is rather different from the others. This B-Corp business has launched four crowdfunding platforms that make a positive social impact.

FundRazr is a digital fundraising platform for non-profits, social causes and professional fundraisers.

Crowdfundr is a platform designed for creators to sustainably fund their projects and ideas.

Cocopay enables friends and family to pay for a patient’s medical costs and quality healthcare.

PetFundr is a crowdfunding platform for animal and pet care for rescues, veterinarians and “pet parents.”

They also provide the backbone technology for organisations to power their own crowdfunding project with an entire advanced fundraising suite.

Between them, these BOLD Awards crowdfunding category finalists display the diversity and versatility of crowdfunding to be applied to worthy public causes, personal needs, pre-orders to support the development of new products, and equity investment in privately-owned businesses, whether they are startups or well established businesses.

There are also several ways a crowdfunding project can be promoted to improve the likelihood of success. On top of developing innovative products and services, they include gaining industry awards; building large social media followings; achieving sales success and satisfied customers; and having lucrative corporate contracts.

Non-finalists can request a VIP Invitation to attend the BOLD Awards gala dinner award ceremony in Lisbon. It’s a unique event for networking with inspiring global innovators, disruptors and entrepreneurs on Friday 28th March. Hope to see you there!

To discuss your own ideas and plans for a crowdfunding project with an independent UK crowdfunding adviser, who is not tied to any specific platforms, start by emailing me at [email protected]. Go on, #beBOLD

Crowdfunding in Europe has already achieved a significant level of growth, adoption and maturity. Various forms of crowdfunding now offer a wide variety of opportunities for Europeans to pursue a range of financial and community-minded/philanthropic aims. Here is a review of equity crowdfunding platforms in Europe, including some niche ones that show how this alternative finance sector is developing in specialist ways.

What is equity crowdfunding?

This form of crowdfunding enables founders of privately-owned businesses to raise funding through selling equity in their company. It is particularly useful for businesses that are at a pre-trading stage with no income because they are unable to qualify for loans, and for businesses seeking modest investment levels that are often too low for venture capitalists to be interested. One of equity crowdfunding’s great benefits to the companies raising funds is that if a business fails the owners do not have to repay equity investments, though it comes with high risks for investors: only one in ten new businesses last ten years or more. Yet successful ones can provide investors with exceptionally high levels of return.

The Americans have arrived in Europe

In the UK the equity crowdfunding sector is dominated by Crowdcube and Republic Europe (formerly Seedrs), which between them have more than an 80% share of the UK equity crowdfunding market. Republic Europe is a recent rebranding of the Seedrs platform since being acquired by the US platform Republic, and exemplifies US expansion in to the European market. Both the UK platforms have European offices that are authorised under European Crowdfunding Service Provider Regulations (ECSPR) to run cross-border fundraising projects throughout the full European Union.

Since February 2023, another US equity crowdfunding platform, Wefunder, operates a pan-European platform which is based in The Netherlands. As in the United States, Wefunder EU enables retail investors to invest in privately-owned businesses alongside angel investors and venture capital funds.

Opportunities to crowdfund across almost the whole continent in single projects, and the arrival of US players, has put pressure on the smaller platforms and the industry is entering a period of consolidation through mergers and acquisitions. The European Crowdfunding Market Report 2023, released in January 2024, informed us that 42% of equity platforms expected to either merge with another platform or be acquired by another platform in the near future.

Impact investing

At the same time, more platforms are trying to carve out a unique marketplace niche. ECSPR provides tremendous opportunities for platforms that were previously restricted to operating within national boundaries to flourish if they can add the right types of investor to their network throughout the whole European Union plus the EEA (European Economic Area).

Platforms that have focussed on particular industry sectors include the French platform We Take Part, which is dedicated to supporting cleantech and climatetech startups. It bridges the gap between entrepreneurs and investors through highlighting innovations that contribute to a sustainable and resilient future. Similarly, Invesdor Group, originally from Finland and now operating across Scandinavia, the UK, and German speaking Austria and Switzerland as well as Germany itself, has positioned itself as an impact investing platform. It offers equity investments and loan opportunities through bonds. Italy’s Ecomill is another equity crowdfunding platform dedicated to energy transition and sustainability.

One key aspect of such impact investments is that backers are seldomly concerned only with a financial return on their investment. They also gain a personal reward from knowing their investment decisions are making a contribution to social and environmental benefits, on whatever scale they may be.

Wider investment opportunities

Some platforms have moved away from a sole focus on crowdfunding as a way for privately-owned business to raise investment budgets. In the UK, both Crowdcube and Republic Europe have developed secondary markets where buyers and sellers can trade shares in private companies that they did not originally acquire through either of the platforms.

With more than 80,000 investors and total investments of over €50m, the German equity-based crowdfunding platform Companisto has several renowned business angels, corporate finance specialists, and venture capital companies in its network.

Sowefund, in France, works with VCs to provide startups with funding from a far smaller “crowd” of more institutional investors. In the UK the SeedLegals platform operates in a similar fashion with a network of angel investors, family funds and VCs. The Envestors platform based in the UK has a network of only high net worth personal investors who sign up to invest significant amounts each year.

Mamacrowd is a leading equity platform in Italy.

In the Republic of Ireland, equity crowdfunding is dominated by the Spark Crowdfunding platform, which began in 2018. However, since May 2023 the Irish-based venture private equity group VentureWave has owned a majority stake in the Estonian platform Funderbeam, which has moved more towards the institutional VC, family funds and angel investor sector.

In Belgium, on the other hand, the Spreds platform (formerly MyMicroInvest), continues to focus on equity and loan crowdfunding for early stage businesses planning to raise between €50,000 and €1,000,000. The platform fully believes in the multi-faceted power of the crowd to help validate a business concept and demonstrate consumer interest, while experienced investors help to examine the valuation of a company and the potential returns on investment.

Investing outside Europe

There are platforms that provide European-based investors with cross-border opportunities to diversify their investment portfolios through acquiring equity in startups, or lending to micro-businesses, in developing economies.

Crowdinvest in the UK is a good example: it features equity investment opportunities in tech startups in developing economies, including India. Built on Web3, tokenised cross-border transactions are made using blockchain technology.

LendaHand in The Netherlands raises funds across Europe to facilitate loans to small and micro-businesses in developing economies.

Platform regulation

Equity crowdfunding platforms have to meet strict legal requirements and complete a thorough Due Diligence process for each project they host. They are regulated by financial authorities, such as the Financial Conduct Authority in the UK, its equivalent in each other country in Europe, and the European Securities and Markets Authority (ESMA) for platforms trading under ECSP Regulations across the whole European Union and the EAA.

There are several online platforms that allow non-high net worth investors to purchase shares or fractional ownership in high-value assets like luxury watches, art, cars, wine, and whisky. These platforms make it possible for everyday investors to diversify their investment portfolios and participate in the ownership of assets that would otherwise be beyond their reach, and for which they may feel a personal passion. The assets often become the property of a ring-fenced individual company, owned by crowds who acquire equity in the various companies.

Like any investment, there’s a risk of loss, especially since these assets can be more volatile or influenced by market trends. Many of these assets also require a long-term holding period to realize their potential appreciation. During such an extended time, these investments are often less liquid than traditional stocks or bonds, although some platforms do offer a secondary market for trading. There can also be costs for safeguarding these assets that would not be applicable to investing in company equity. Blockchain and NFT technology are making an impact in this sector.

A leading source of data on fractional ownership investment performance is the Knight Frank Luxury Investment Index (KFLII), which tracks the performance of 10 popular “investments of passion.”

Knight Frank’s Luxury Investment Index Q4 2023

Asset class

12-month price change (%)

10-year price change (%)

Art

11%

105%

Jewellery

8%

37%

Watches

5%

138%

Coins

4%

56%

Coloured diamonds

2%

8%

Wine

1%

146%

Furniture

-2%

40%

Handbags

-4%

67%

Cars

-6%

82%

Whisky

-9%

280%

Here are some relevant platforms. I have chosen a cross-section to show the range of what is available.

Konvi

Konvi is a pan-European crowdfunding platform, based in Dublin, Ireland, for people to invest through shared ownership of luxury items like watches, art and fine wines. A holding company is created for every asset that is going to be funded. This holding company and its purpose is to own, manage, and sell that one particular asset. When a person invests in an asset, they become a shareholder in this holding company. Konvi was founded in 2020,

ARTSPLIT

ARTSPLIT allows retail investors to buy fractional shares in high-value artworks. The platform, which is based in Paris, France, selects and acquires pieces from established and emerging artists, offering them as “Splits” to investors who can purchase shares. Investors can choose from a curated collection of artworks, which are professionally valued, insured, and stored. This allows retail investors to own a portion of blue-chip and contemporary art without the need to invest large sums of money.

The minimum investment can vary but typically starts from as low as €50 per share, making it accessible for a wide range of investors. ARTSPLIT offers a secondary market where investors can trade their shares. This means investors can buy or sell their shares in the artworks with other investors on the platform, providing flexibility and potential liquidity.

Wine Owners

This platform is based in London, and has a focus on fine wine and spirits. It operates as both an investment and a wine portfolio management platform. Investors can buy, sell, and manage wine collections with the platform acting as a marketplace. The minimum investment varies depending on the specific wine but often starts around a few hundred pounds. It is ideal for wine enthusiasts and investors looking to directly own bottles of fine wine or build a diversified portfolio.

CaskX

This platform specialises in whisky casks from leading distilleries in Scotland and the US. Investors can purchase entire casks or fractions of whisky casks, with the option to let them age or sell when the value appreciates. Its head office is in California, though it also has an office in Scotland.

WiV Technology

WiV Technology is based in Oslo, Norway, and offers fractional ownership of fine wine and rare spirits. It uses blockchain technology to tokenize fine wine assets, enabling secure trading. Investors can purchase shares in individual bottles or cases of wine, and the platform offers full traceability and provenance verification. The minimum investment starts at around €50, and there is a secondary market where investors can trade wine tokens, providing liquidity. It is ideal for investors interested in combining blockchain technology with fine wine investment.

A look to the future of crowdfunding in Europe

I will leave the final words to the European Crowdfunding Network. It seeks to align crowdfunding with the new European Commission’s vision for sustainable growth

“As Europe advances its sustainability and digital innovation goals, crowdfunding can play a pivotal role. Platforms are already facilitating direct investments in renewable energy projects, circular economy initiatives, and technological start-ups, directly supporting the EU’s green and digital transitions.

Crowdfunding is also an important tool for fostering democratic engagement in the economy. By allowing European citizens to invest directly in securities or loans for businesses, crowdfunding offers a transparent and participatory model for financial inclusion. Though small in scale compared to institutional mechanisms, crowdfunding enables bottom-up economic participation that aligns with the EU’s ambition to strengthen social cohesion and economic resilience.”

For 10 years I have been an independent crowdfunding advisor, with no attachments to any particular platforms. If you have crowdfunding ideas or plans you would like to discuss with someone who can give objective views and support, please get in touch through [email protected].

It is a very helpful that many people who have been successful at using crowdfunding are prepared to share their tips and insights. This article includes some crowdfunding tips offered by four experienced users.

Due Diligence is often problematic

John Auckland of Tribe First, which provides crowdfunding “boot camps,” shared in a radio show that information given in team biographies often delays the crowdfunding due diligence process more than any other section of the pitch. Every claim has to be evidenced, including the management team’s career history with payslips and tax returns. It’s a challenge and failing due diligence checks can significantly delay a campaign. Rather than deliberately trying to mislead anyone, failure is often because people don’t have the evidence to hand for the claims being made.

“It might sound impressive that you made 10,000 sales last month, or achieved a 300% sales growth in just one year, but can you demonstrate it? If you’re making claims like this, you’ll have to offer the platform a complete list of your sales and show your working.” Source: John Auckland on Kent Business Radio.

After publishing this article, and in his role as CEO of Seafields Solutions, John Auckland and his team went on to secure a total of £2.9 million in funding comprising equity, debt, grants, and donations in March 2025. Seafields’ primary focus is on developing offshore aquafarms to grow large amounts of biomass for carbon dioxide removal. The March 2025 total included £92,262 through equity crowdfunding from 274 investors. Seafields Solutions had also previously raised £522,859 from 683 equity crowdfunding investors in 2023.

The close attention paid to Due Diligence is corroborated by Chris Forbes, co-founder of The Cheeky Panda. The Cheeky Panda is a brand of tissues and related products made from sustainable bamboo, not paper (which is essentially from trees). “Entrepreneurs should keep in mind that due diligence is probably the most arduous part of the [crowdfunding] process. You’ll need appropriate evidence for every claim you intend to make in the pitch.” Source: Republic Europe (formerly Seedrs) case study.

Good crowdfunding is good marketing

Chris Forbes additionally shared that each of The Cheeky Panda’s equity crowdfunding rounds was also valuable for brand awareness and PR that lasted long after the rounds closed.

The business now has over 1,800 shareholders who are also avid supporters and who continue to advocate for, and positively impact the brand.

Every one of the shareholders can be extremely helpful, which is why he ensures that every effort is made to be as communicative and transparent as possible, even after the round has closed, to make sure that no inquiries go unanswered and to take the insights of shareholders on board.

Crowdfunding’s advantages over VC funding

Laurence Kemball-Cook is CEO of Pavegen, an innovative B2B company that generates sustainable electricity from people’s footsteps. In an explanation of why he chose to use crowdfunding to raise early-stage investment, he said the terms from VCs are always restrictive. “They want board seats, control, liquidation preferences, restrictive terms on the founders – all things which don’t favour the company raising money,” he explained in an interview.

Much of this is echoed by Chris Forbes of The Cheeky Panda. “For the last round [of equity crowdfunding] we spoke to a lot of Private Equity houses but they tend to be slower-moving, and we wanted to expedite the process. We didn’t want to give up large percentages of equity, end up with a mix of equity and debt, or undergo expensive board hires which would compromise our profitability. We also didn’t want to be instructed how to spend the funds by external parties. We prefer to do things our way, and the crowd supports that.”

Have a communications strategy

Patrick Dumas is co-founder of Square Mile Farms, a vertical farming business created to bring farming to urban spaces, boosting wellbeing and sustainability. He found that crowdfunding is a very busy, stressful and distracting process. A key learning for their second round of equity crowdfunding, and one of his crowdfunding tips to make it less stressful and more manageable, is to have a clear communication strategy to follow. This included LinkedIn and email outreach from the pre-registration stage onwards. They were more organised and proactive with their communications the second time, with a schedule list to work from.

Like The Cheeky Panda, Square Mile Farms has over 1,000 shareholders from crowdfunding, and the feedback they’ve had from them is overwhelmingly positive, constructive and straightforward, Patrick said in a case study. They issue quarterly updates, and occasionally people respond to them with a lead or recommendation, which they find really helpful.

After immersing myself in crowdfunding for almost ten years I have a few crowdfunding tips and insights of my own. Please get in touch via [email protected] if you have crowdfunding ideas or plans you’d like to discuss.

Of the crowdfunding campaigns and related news I noticed in October there was a high proportion that were food related. This includes startup food brands and restaurants. Entrepreneurs and startup founders in these sectors have identified that as well as raising funds to invest in the business, well planned and executed crowdfunding also represents good marketing.

Crowdfunding for food and drinks brands can stimulate trial, prompt consumers to ask for them in their local outlets, and increase brand loyalty among existing users who can become investors. New shareholders can also become valuable customers in a virtuous circle that gives crowdfunding backers a strong motivation to become brand advocates and ambassadors.

Similarly, crowdfunding used by restaurants can bring forward consumer demand and have them pay now for meals they will enjoy at a later date. From burger and coffee chains to Michelin-starred restaurants, it provides customers with a talking point to recommend a favourite place to go to friends and colleagues. Perks such as limited places for cookery lessons, or even meals prepared by chefs in crowdfunding backers’ own homes can deliver a wow-factor to make the backers feel special, and once again give them a talking point.

Crowdfunding backers also have the chance to get to know about the people behind startup food and drink brands, and restaurants, and maybe identify with their broader aims from an increasingly ESG or community asset perspective.

Crowdfunding by Restaurants

Chefs Lewis Dwyer and Andy Aston opened their independent Michelin Star restaurant called Hiraeth in Cowbridge, Wales, last November after raising £30,000 of reward-based donations through crowdfunding. They now need new premises after the landlord unexpectedly decided to sell the property.

Chef Merlin Labron-Johnson had already beaten his £125,000 crowdfunding target with 10 days left to run. He was raising money to relocate his farm-to-table restaurant Osip 2.0 in Somerset. His crowdfunding went on to achieve £166,261 from 464 backers to help bring this project to life. As perks, he offered branded restaurant crockery, chocolate cookie tasting sessions, hampers of mixed goodies, lunch and dinner at the restaurant for groups up to eight people, and home cooked meal for fifteen, and tickets for an exclusive opening night party.

Equity crowdfunding by London-based Honest Burgers’ closed after raising almost £3m. The casual dining restaurant group soundly beat its £1m target, raising £2,905,631 from 3,456 investors. It will now open further restaurants and launch a new quick-service burger.

Founded in Barcelona in 2020, startup coffee chain GoodNews is soon launching a round of equity crowdfunding after three previous seed and Series A funding rounds, which have already raised €15m (£13m). Good crowdfunding can be good marketing and attract loyal customers.

Startup founders Florin Grama and Felix Ortona Coles met while working at St Barts restaurant in London’s Smithfield Market area. In October they began reward-based crowdfunding to raise £20,000 for the final pieces of equipment they needed to open their Tarn Bakery in Highgate. Perks include classes to make croissants, sourdough pastry and pasta. By October 29 they had reached £15,242 with eight days left to run.

Crowdfunding by food and drink startups

With the growing demand for minimally processed and natural plant-based food, Tempeh brand Better Nature has launched another round of equity crowdfunding as part of a £1 million-plus raise to drive retail growth for its meat alternative range across the UK and Europe.

Hertfordshire-based SRSLY Low Carb has signed an agreement with a food distributor that services leading supermarket chains in all 50 US states. To support global growth, SRSLY is embarking on a seven-figure equity investment round which includes a round of equity crowdfunding in November with a minimum target of £500,000.

Earlier this year, craft beer maker Gipsy Hill Brewing in southeast London launched the world’s first carbon-negative beers, achieved without relying on carbon offsets. A new crowdfunding campaign in November will help them accelerate their climate-positive agenda. The brewery ran its first equity investment round in 2022, in which 581 investors joined its community and invested £865,149, 130% above Gipsy Hill’s target.

A former City analyst founded the Cheesegeek food marketplace platform in 2017 to connect artisan cheesemakers with consumers. Edward Hancock now hopes his equity crowdfunding campaign in November 2023 will raise £150,000 so he can start a forum for cheese fans, with investors invited to develop a new variety.

French plant-based food brand La Vie closed its equity crowdfunding in October with 2,691 backers investing €2.1 million. La Vie, whose UK headquarters are in London, used the Crowdcube platform which through its Barcelona office is authorised to run crowdfunding campaigns throughout the EU as well as in the UK. La Vie’s multi-award-winning plant-based alternative to bacon is available in 13 European countries. The brand claims to have so far saved over 90,000 pigs and 2 million tonnes of CO2.

Considering crowdfunding?

If you are thinking about running crowdfunding, and in any sector, not just crowdfunding for food brands, the most common mistake is to not allow enough time for preparatory work. This can include building larger networks of followers, and for those considering equity crowdfunding the platforms will require you to have lead investors prepared to guarantee a minimum of 30% of your target raise.

I am an independent crowdfunding strategist and adviser, unattached to any particular crowdfunding platforms. Please get in touch for objective advice and insights into your plans, and maybe hands-on support if you decide you want it. Send an email to [email protected] to get started.

There are different types of crowdfunding, and plenty of platforms to choose from for generating donations to a charity or a worthy cause; asking for help to complete new product development; personal fundraising, such as for medical costs or educational fees; accessing loans at lower-than-high-street interest rates; buying and selling shares in privately-owned businesses; and using a crowdfunding platform as a distribution channel to generate pre-paid product orders. The choice of a crowdfunding platform can significantly impact the success of a campaign, particularly for startups seeking business finance. So it’s important to carefully consider the following 15 criteria for choosing which crowdfunding platform to use.

Type of Crowdfunding: There are different types of crowdfunding, including donation-based, reward-based, equity-based, and lending-based crowdfunding. Choose a platform that aligns with the type of crowdfunding you’re looking to use for your campaign.

Fees and Costs: Crowdfunding platforms usually charge fees for hosting campaigns on their platform. These fees can vary significantly and may include platform fees, payment processing fees, and other charges. Evaluate the fee structure to understand how much of your funds will be used to cover these costs.

Target Audience and Niche: Some platforms cater to specific niches or industries. Choose a platform that attracts backers who are interested in your project’s field or sector.

Geographic Reach: Consider the platform’s global reach and the countries where it operates. Some platforms are more popular in certain regions, so choose one that aligns with your key target audience’s location.

Platform Reputation and Trustworthiness: Research the platform’s reputation, history, and success stories. Look for reviews from other campaigners to gauge the platform’s reliability and trustworthiness. Platforms that are members of the UK Crowdfunding Association are obliged to follow the UKCFA Code of Conduct.

User-Friendly Interface: A user-friendly platform with an intuitive interface can make it easier for both campaigners and backers to navigate and participate.

Campaign Support: Check if the platform provides resources, guides, and customer support to help you create and manage your campaign effectively.

Visibility and Exposure: Some platforms have a larger user base and better marketing reach, which can increase the visibility of your campaign. Consider the platform’s ability to help your campaign reach a wider audience.

Fund Disbursement: Understand the platform’s policies regarding how and when funds will be disbursed to you. Some platforms release funds only after the campaign reaches its funding goal, while others may allow earlier partial disbursements.

Flexible Funding Options: Some platforms offer flexible funding, where campaigns receive the funds even if they don’t meet their target goal. This is known as Keep What You Raise. Others use an All-or-Nothing approach. Choose the one that aligns with your campaign strategy and your available budget to run your crowdfunding. You don’t want to incur costs and then realise you aren’t going to have any money.

Social Sharing and Integration: Look for platforms that have social sharing features and integrations with social media platforms. This can help your campaign gain traction through online sharing.

Analytics and Reporting: Consider platforms that provide analytics and reporting tools to help you track the progress of your campaign and understand your backers’ behaviour.

Legal and Compliance: Different crowdfunding models have legal and regulatory implications. Ensure the platform complies with relevant laws and regulations for your type of campaign.

Intellectual Property Protection: If your campaign involves a product or innovation, research how the platform handles intellectual property protection to safeguard your idea.

Community and Engagement: Platforms with active communities and engaged backers can provide valuable feedback and support for your campaign.

Ultimately, choosing a crowdfunding platform should align with your campaign’s goals, target audience, and the type of crowdfunding you’re using. Carefully review your options and choose the platform that best suits your needs. If you want some help, I am an independent crowdfunding advisor with no ties to any particular platform. Send me an email to [email protected]. Or follow me on Twitter where I regularly post news about crowdfunding campaigns.

The main image shows some of the crowdfunding platforms available to use in the UK – apologies to the ones I have left out.

Many startups using crowdfunding offer techie apps or fintech products and services, but it was a Midlands-based doughnut company that recently enjoyed phenomenal equity crowdfunding success.

The Project D doughnut company, set up in 2018 by three former schoolmates, launched an equity crowdfunding campaign in May 2023 to raise £400,000 and accelerate the company’s growth. It already had an annual turnover of £2.6m prior to the crowdfunding, and had set an aim to reach £12 million in three years. They were staggered to receive, in just a preliminary private investment round, pledges of £2 million. This was before it was even open to the general public. They used the Crowdcube platform, which is a major one for equity crowdfunding offers in the UK.

The three founders were left wondering how to respond: how much added equity would they open up to crowdfunding investors? Some people may think they should just take the full £2m on offer from investors in the private round, and then go ahead and generate even more from the public round. However, given the high demand for their equity, they could scale back now and possibly come back soon with another round at a higher share price.

Equity crowdfunding success like this is great to see, though it doesn’t happen very often to this degree. And it does also present some problems. I began to think about what the reasons or the circumstances were that caused this surge of popularity. Five factors came to mind.

1. Project D has a low-entry-cost product that significant numbers of customers have been able to try, and evidently decided they like the doughnuts and the way the company operates its D2C order-taking and delivery. They have a substantial community of over one million people to attract as investors. They had obviously done some good data capture work to be able to communicate the crowdfunding offer to them.

2. A lead investor had guaranteed £150,000 – 37.5% of the initial £400,000 target. That gives smaller investors confidence to go ahead.

3. The business had used social media very cleverly to raise brand awareness, with viral videos on its Tiktok account receiving 19 million views in a single two-month period.

4. Project D can claim corporate accounts with British Airways, Brewdog, Amazon and Rolls-Royce. It might have been no more than a delivery to a local office, but big brand names add cachet and boost investor confidence.

To investors, it must have looked like a tasty winner all the way! There are lessons here for all sorts of companies in many different sectors about customer data capture, effective marketing, the value of corporate accounts and the reputational benefits of entering and winning awards.

If you are considering running a business-related crowdfunding project, and want to discuss it with an independent crowdfunding adviser, then please get in touch by an email to [email protected]. To keep up with crowdfunding news, events and projects you can follow me on Twitter.